diff --git a/docs/examples/finance-chart-sandbox/README.mdx b/docs/examples/finance-chart-sandbox/README.mdx

index 62ee87c..47bf972 100644

--- a/docs/examples/finance-chart-sandbox/README.mdx

+++ b/docs/examples/finance-chart-sandbox/README.mdx

@@ -1,42 +1,43 @@

---

title: Finance Chart (Sandbox)

-description: Chart a stock's closing-price history with the Perplexity Agent API sandbox tool — fetched and built inside an isolated container as a background task, then rendered locally.

+description: Chart a stock's closing-price history with the Perplexity Agent API sandbox tool — the sandbox fetches the prices and renders the chart inside an isolated container, returning the CSV and PNG as downloadable files.

sidebar_position: 8

-keywords: [agent-api, sandbox, code-execution, stock-chart, matplotlib, csv, background]

+keywords: [agent-api, sandbox, code-execution, file-creation, stock-chart, matplotlib, csv, png, background]

---

# Finance Chart (Sandbox)

A command-line tool that charts a stock's closing-price history using Perplexity's [Agent API](https://docs.perplexity.ai/docs/agent-api/quickstart) [`sandbox`](https://docs.perplexity.ai/docs/agent-api/tools/sandbox) tool.

-The whole agent loop runs inside **one background Agent API request**:

+Everything runs inside **one background Agent API request**:

-1. The model is given the `sandbox` tool — a full agentic Python environment that includes the Perplexity SDK (web search + URL fetch).

-2. Inside the sandbox it finds and fetches the ticker's historical daily closing prices, parses them, and prints a clean `date,close` CSV to stdout between sentinel fences.

+1. The model is given the `sandbox` tool — a Python environment with `urllib`/`pandas`/`matplotlib` and a writable working directory.

+2. Inside the sandbox it fetches the ticker's daily closing prices from a **pinned data source** (Yahoo Finance's v8 chart JSON endpoint), **writes `prices.csv`**, and **renders `chart.png`**. The sandbox exposes both files as downloadable **artifacts**.

-The script polls the request to completion, pulls the CSV out of the sandbox's stdout, saves it, and renders the line chart **locally** with matplotlib.

+The script polls the request to completion and downloads both files — no local rendering, so it has no third-party dependencies.

-

+

## How it differs from the docs (important)

This recipe was built and verified against the live Agent API. A few realities shape the design:

- **The `sandbox` tool requires a background task.** On the synchronous/streaming path the request is rejected with `streaming failed: ... unknown tool "sandbox"`. You must submit with `background: true` and poll the response by id. This script always does that.

-- **`stdout` is nested.** The execution output lives at `sandbox_results.results[].stdout`, not at the top level of the `sandbox_results` item.

-- **`finance_search` has no history (current deployment).** The top-level `finance_search` tool returns only the latest quote, so the price *series* is gathered from inside the sandbox using its in-container Perplexity SDK.

-- **Sandbox data fetching is best-effort.** Because the sandbox pulls from third-party web sources, requests can be rate-limited. The script retries the whole call a few times (`--attempts`) until it gets a usable CSV.

-- **No PNG comes back.** `sandbox_results` carries only text, so the chart is rendered client-side — and you keep a reusable `.csv`.

+- **The sandbox returns files.** Anything the sandbox writes to its working directory comes back as a `share_file` output item carrying a `file_id`, `filename`, and a ready `/v1/responses/{id}/files/{file_id}/content` URL — you can also list them with `GET /v1/responses/{id}/files`. The script downloads the `prices.csv` and `chart.png` artifacts directly, instead of scraping anything out of `stdout`.

+- **Pin the data source to cut latency.** The slow part of an unconstrained sandbox run is the model *hunting* for a price source (public pages `429` or gate behind captchas — easily 3–7 sandbox calls). Telling it to hit Yahoo's v8 chart JSON endpoint directly turns that into a **single** fetch, and leaves token budget to render the chart in the same session. A typical run is now **one sandbox invocation**.

+- **Give the sandbox output-token headroom.** The sandbox spends `max_output_tokens` *writing the code* that fetches the data and renders the chart. A tight cap can starve the file-writing step (the data gets fetched but the files are never written). This recipe uses `8192`.

+- **`finance_search` has no history (current deployment).** The top-level `finance_search` tool returns only the *latest quote* — a single row — so it can't produce a price *series*. The history is fetched inside the sandbox instead.

+- **Sandbox data fetching is best-effort.** Even a pinned source can rate-limit; the prompt falls back to a second source (Stooq), and the script retries the whole call a few times (`--attempts`).

The Agent API is called over **raw HTTP** (stdlib `urllib`, no SDK) so the exact request body is visible and the endpoint is configurable.

## Features

- One background request orchestrates the sandbox; the script polls it to completion (resilient to transient 5xx)

-- Sandbox fetches the price history itself and emits a fenced `date,close` CSV; the script extracts it from `sandbox_results.results[].stdout` (with message-text fallbacks)

-- Automatic retries until a usable CSV is parsed

-- Renders a clean closing-price line chart with matplotlib (headless `Agg` backend)

-- Saves both a reusable CSV and a PNG

+- The sandbox **fetches the prices and renders the chart itself**, writing a `date,close` CSV and a PNG; the script reads the `share_file` artifacts off the response and downloads them (falling back to the `/files` endpoint)

+- Pinned data source (Yahoo v8 chart JSON, Stooq fallback) keeps it to ~1 sandbox call

+- Automatic retries until both files come back and the CSV parses

+- No third-party dependencies — the chart is rendered server-side, in the sandbox

- Configurable `--base-url` / `PERPLEXITY_BASE_URL`; reports sandbox invocation count and request cost

## Prerequisites

@@ -48,7 +49,8 @@ The Agent API is called over **raw HTTP** (stdlib `urllib`, no SDK) so the exact

```bash

cd docs/examples/finance-chart-sandbox

-pip install -r requirements.txt # matplotlib only — the API is called over raw HTTP

+# No dependencies to install — the API is called over raw HTTP and the chart is

+# rendered inside the sandbox. (requirements.txt is intentionally empty.)

chmod +x finance_chart_sandbox.py

```

@@ -74,7 +76,7 @@ This writes `AAPL_6mo.csv` and `AAPL_6mo.png` to the current directory.

```bash

./finance_chart_sandbox.py TICKER [--period 6mo] [--start YYYY-MM-DD --end YYYY-MM-DD] \

- [--model MODEL] [--attempts 3] [--max-steps 25] [--poll-timeout 300] \

+ [--model MODEL] [--attempts 3] [--max-steps 15] [--poll-timeout 300] \

[--out-dir DIR] [--base-url URL] [--api-key KEY] [--keep-json]

```

@@ -99,22 +101,22 @@ PERPLEXITY_BASE_URL=https://api.perplexity.ai ./finance_chart_sandbox.py NVDA

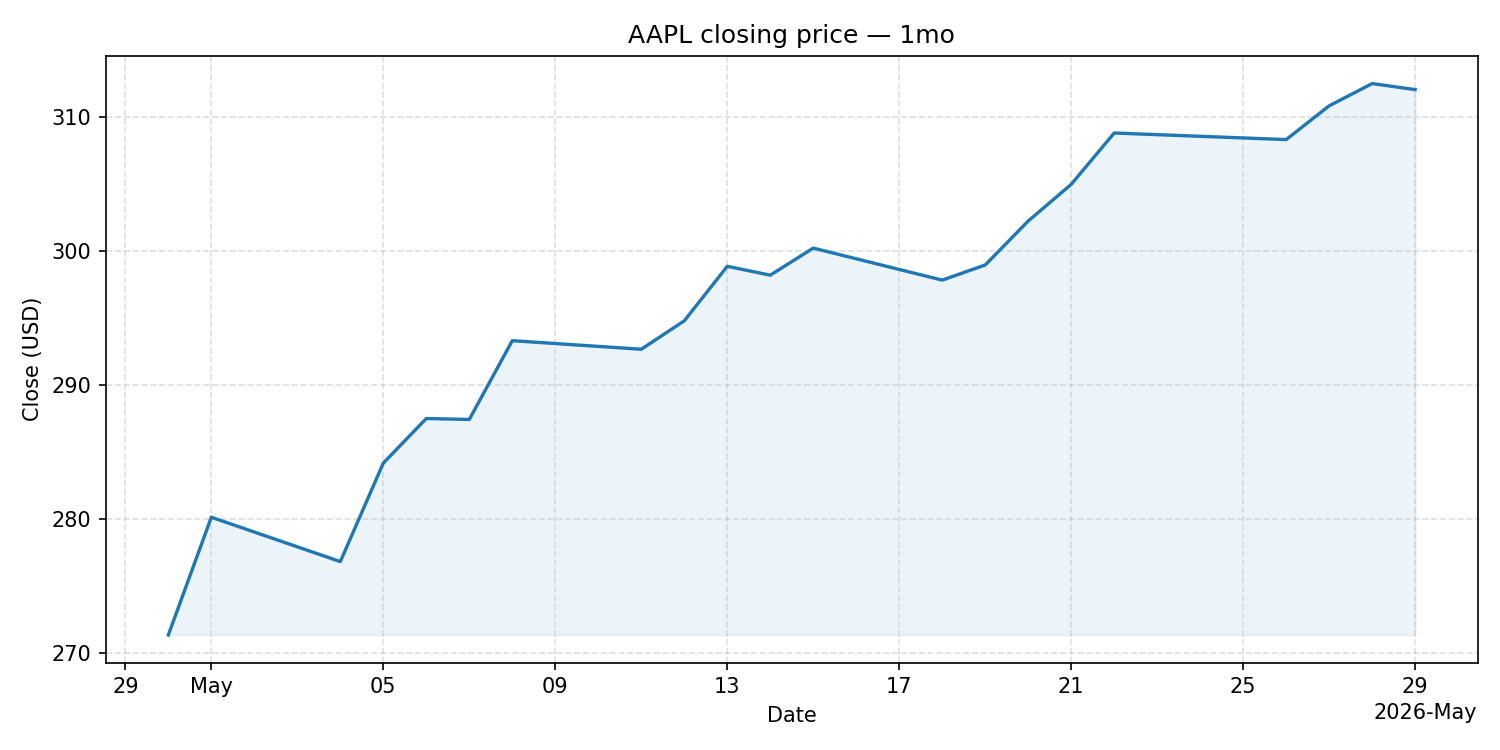

## Example Output

```

-[attempt 1/3] Asking the sandbox to fetch AAPL closing prices over the past 1 month...

+[attempt 1/3] Asking the sandbox to fetch AAPL closing prices over the past 1 month and plot them...

-Data points: 21 (2026-04-30 → 2026-05-29)

+Data points: 21 (2026-05-08 → 2026-06-08)

CSV: AAPL_1mo.csv

-Chart: AAPL_1mo.png

-Sandbox invocations: 8

-Cost: 0.3509 USD

+Chart: AAPL_1mo.png (fetched and rendered in the sandbox)

+Sandbox invocations: 1

+Cost: 0.1003 USD

```

The CSV (`AAPL_1mo.csv`):

```csv

date,close

-2026-04-30,271.35

-2026-05-01,280.14

-2026-05-04,276.83

+2026-05-08,293.32

+2026-05-11,292.68

+2026-05-12,294.80

...

```

@@ -124,17 +126,19 @@ date,close

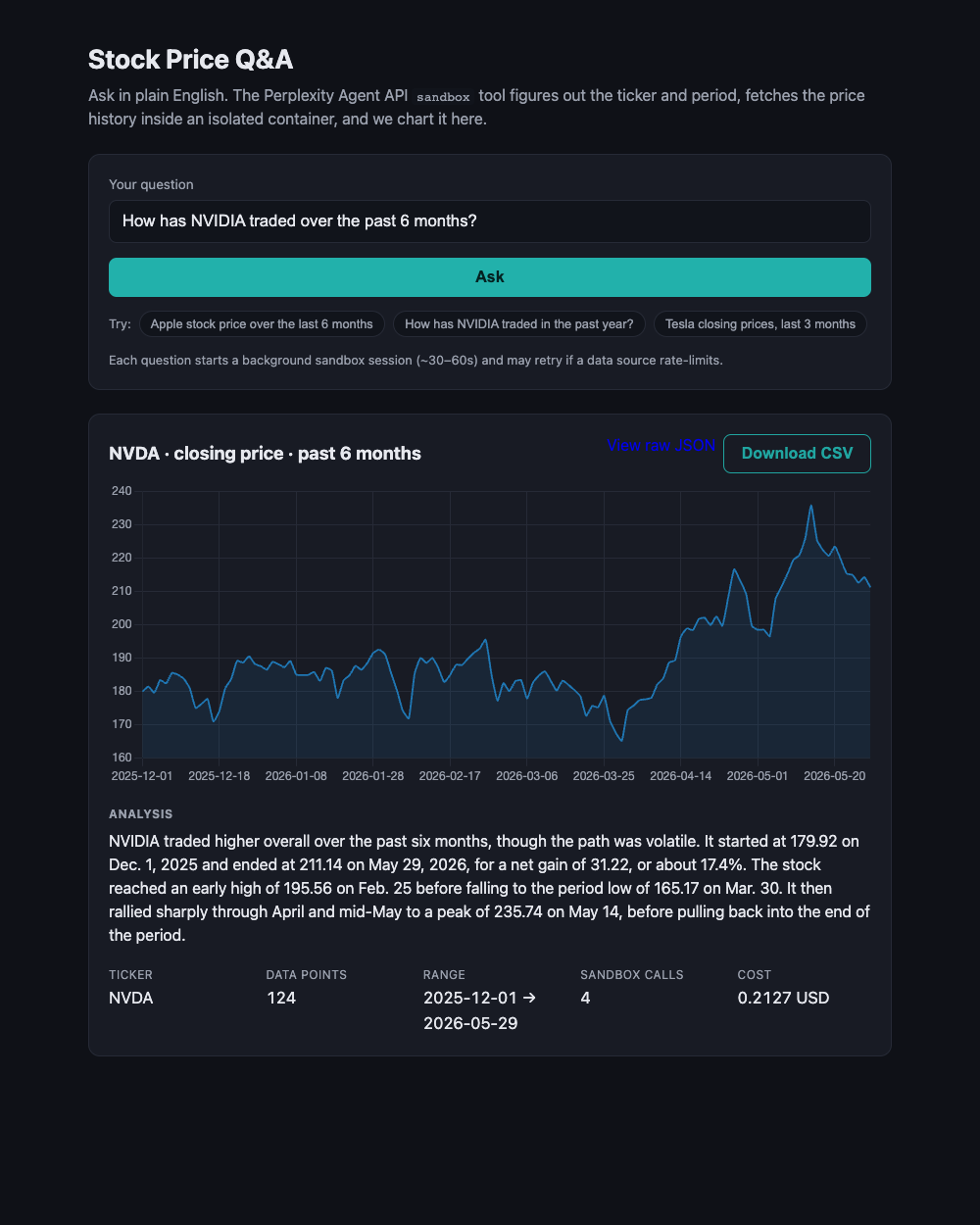

A small web app in [`webapp/`](webapp/) puts a **natural-language** front door

on the agent loop: ask *"What was Apple's stock price over the last 6 months?"*

-and the model resolves the ticker and period itself, fetches the prices in the

-sandbox, and the page charts the result.

+and the model resolves the ticker and period itself, fetches the prices and

+renders the chart in the sandbox, and the page shows the result.

Unlike the CLI (which calls the API over raw HTTP), the web backend uses the

-**Perplexity Python SDK** and reuses the CLI module's CSV-extraction and parsing

+**Perplexity Python SDK** and reuses the CLI module's parsing and shared-file

helpers. It runs a **two-phase** flow, because the `sandbox` tool only runs as a

(non-streamable) background task:

1. **Data** — a background call (`client.responses.create(..., background=True)`

then `client.responses.retrieve(id)`) where the sandbox resolves the ticker +

- period, fetches the prices, and prints a `META`/`CSV` block.

+ period, fetches the prices, **writes `prices.csv` and renders `chart.png`**

+ (both downloaded by the backend), and prints a tiny `META` block for routing

+ (ticker + label).

2. **Answer** — a separate **streaming** call (`stream=True`) that writes a short

natural-language analysis of the series, token by token.

@@ -142,16 +146,17 @@ helpers. It runs a **two-phase** flow, because the `sandbox` tool only runs as a

| --- | --- |

| `POST /api/charts` | Submit a question (`{query, attempts?}`) → returns a `job_id` |

| `GET /api/charts/{job_id}/events` | **Server-Sent Events**: `progress` → `chart` → streamed `token`s → `done` |

+| `GET /api/charts/{job_id}/chart.png` | The chart PNG the sandbox rendered |

| `GET /api/charts/{job_id}/response.json` | The **raw Agent API response** from phase 1 (sandbox code, stdout, usage) |

| `GET /api/charts/{job_id}/csv` | Download the `date,close` CSV |

The job runs in a worker thread and writes incremental state onto the job; the

SSE endpoint merely *tails* that state, so reconnects never re-run the work. The

-frontend (vanilla JS + [Chart.js](https://www.chartjs.org/) from a CDN — no

-build step) renders the chart on the `chart` event, appends the streamed

-analysis live, and links to the raw JSON for inspection.

+frontend is vanilla JS with **no build step and no charting library** — on the

+`chart` event it simply points an `` at the sandbox-rendered PNG, appends

+the streamed analysis live, and links to the raw JSON and CSV.

-

+

### Run it

@@ -164,7 +169,7 @@ python app.py # serves http://127.0.0.1:8000

```

Open the page, type a question (or click an example), and hit **Ask**. The

-status line updates per attempt while the background sandbox runs (~30–60s).

+status line updates per attempt while the background sandbox runs (~20–40s).

## Code Walkthrough

@@ -173,15 +178,18 @@ status line updates per attempt while the background sandbox runs (~30–60s).

```python

payload = {

"model": "openai/gpt-5.5",

- "instructions": SYSTEM_PROMPT, # "print the CSV between fences"

- "input": "Produce the daily closing-price CSV for AAPL over the past 6 months. ...",

+ "instructions": SYSTEM_PROMPT, # "fetch from Yahoo v8, write CSV + render PNG"

+ "input": "Fetch this exact URL ... Write prices.csv and render chart.png for AAPL ...",

"tools": [{"type": "sandbox"}],

"background": True, # required for the sandbox tool

- "max_steps": 25,

+ "max_output_tokens": 8192, # headroom for the in-sandbox code

+ "max_steps": 15,

}

# POST https://api.perplexity.ai/v1/responses (Authorization: Bearer )

```

+The prompt pins the data source (`https://query1.finance.yahoo.com/v8/finance/chart/?range=&interval=1d`, Stooq as fallback) so the sandbox fetches in one shot instead of hunting across rate-limited pages.

+

**2. Poll the response by id until it completes.**

```python

@@ -191,38 +199,40 @@ while body["status"] in ("queued", "in_progress"):

body = get(f"/v1/responses/{body['id']}") # tolerate transient 5xx

```

-**3. Pull the CSV out of the nested sandbox stdout.**

+**3. Find the files the sandbox shared and download them.**

```python

for item in body["output"]:

- if item["type"] == "sandbox_results":

- for res in item["results"]:

- stdout = res["stdout"] # contains the fenced CSV

+ if item["type"] == "share_file":

+ url = item["url"] # /v1/responses/{id}/files/{file_id}/content

+ # item["filename"] is "prices.csv" or "chart.png"

+data = get_raw(url) # Authorization: Bearer

```

-The script searches each `sandbox_results.results[].stdout` for text between the `===CSV_START===` / `===CSV_END===` fences (falling back to the message text and a ```` ```csv ```` block), validates it parses into ≥2 `date,close` rows, and retries the whole call if not.

+The script reads the `share_file` items off the response (falling back to `GET /v1/responses/{id}/files` if none are inlined), downloads both the `.csv` and the `.png`, validates the CSV parses into ≥2 `date,close` rows, and retries the whole call if not.

-**4. Render the chart locally.** The CSV is parsed with the stdlib `csv` module and plotted with matplotlib's headless `Agg` backend. Because the sandbox returns only text, rendering lives on the client side and you keep a tidy `.csv`.

+**4. Keep the files.** The CSV and the sandbox-rendered PNG are written to disk — there's nothing to render client-side, so the CLI has no third-party dependencies. (The CSV is parsed only to report the series length.)

## Prompting Guidance

-- **Fence the machine-readable output.** Asking the sandbox to wrap the CSV in unique sentinel lines makes extraction robust even when the model adds commentary or debug prints.

-- **Tell it to retry sources.** Public price endpoints rate-limit (e.g. Yahoo `429`) or gate behind captchas; instructing the model to try another source on failure improves the hit rate.

+- **Make the files the deliverable.** State plainly that the task is complete only once `prices.csv` and `chart.png` exist in the working directory — otherwise the model may answer with the prices in prose and never write the files.

+- **Pin the data source.** Handing the sandbox the exact fetch URL (Yahoo's v8 chart JSON) collapses a multi-call source hunt into a single fetch — the biggest latency win — and frees up budget to render the chart in the same session.

+- **Give output-token headroom.** The sandbox spends `max_output_tokens` writing the code that fetches the data and renders the chart; with too small a cap it runs out before the write step. `8192` is comfortable.

+- **Name a fallback source.** Even a pinned endpoint can `429`; telling the model to fall back to a second source (Stooq) improves the hit rate.

- **Forbid fabrication.** The system prompt instructs the model to use only prices it actually retrieved — never to interpolate or estimate.

## Pricing

- **`sandbox`**: `$0.03` per container session

-- **In-sandbox SDK search queries**: `$0.005` per request (the sandbox issues these to gather the data)

- **Model tokens**: billed separately per Agent API token pricing

-Sandbox invocations are counted under `usage.tool_calls_details.sandbox.invocation`. A typical run here is a few sandbox calls plus a handful of in-sandbox searches. See [Perplexity Pricing](https://docs.perplexity.ai/docs/getting-started/pricing) for current rates.

+Sandbox invocations are counted under `usage.tool_calls_details.sandbox.invocation`, and file sharing under `usage.tool_calls_details.share_file.invocation`. With a pinned data source a typical run is **one** sandbox invocation (no in-container web searches), which keeps cost low (~`$0.10` in our runs). See [Perplexity Pricing](https://docs.perplexity.ai/docs/getting-started/pricing) for current rates.

## Limitations

- `sandbox` is in **preview** and must be run as a background task

-- Price history is fetched from third-party web sources inside the sandbox, so **data accuracy and availability depend on those sources** — values should be sanity-checked, and obscure/non-US tickers may fail

-- Fetching is **best-effort**: rate limits can cause an attempt to return no CSV; the script retries, but a run may still fail (raise `--attempts`)

+- Price history comes from third-party sources (Yahoo v8 chart JSON, Stooq fallback) fetched inside the sandbox, so **data accuracy and availability depend on those sources** — values should be sanity-checked, and obscure/non-US tickers may fail (Stooq expects a `.us` suffix)

+- Fetching is **best-effort**: rate limits can cause an attempt to return no files; the script retries, but a run may still fail (raise `--attempts`)

- Each attempt is a separate billed sandbox session

- This is not investment advice

diff --git a/docs/examples/finance-chart-sandbox/finance_chart_sandbox.py b/docs/examples/finance-chart-sandbox/finance_chart_sandbox.py

index f3687e4..5d27a30 100644

--- a/docs/examples/finance-chart-sandbox/finance_chart_sandbox.py

+++ b/docs/examples/finance-chart-sandbox/finance_chart_sandbox.py

@@ -1,31 +1,40 @@

#!/usr/bin/env python3

"""

Finance Chart (Sandbox) - Plot a stock's closing-price history using the

-Perplexity Agent API ``sandbox`` tool, then render the chart locally.

+Perplexity Agent API ``sandbox`` tool. The sandbox fetches the prices AND

+renders the chart, returning both as files — no local rendering.

-The agent loop runs entirely inside one **background** Agent API request:

+Everything runs inside one **background** Agent API request:

- 1. The model is given the ``sandbox`` tool — a full agentic Python

- environment that includes the Perplexity SDK (web search + URL fetch).

- 2. Inside the sandbox it searches for / fetches the ticker's historical

- daily closing prices, parses them, and prints a clean ``date,close`` CSV

- to stdout between sentinel fences.

+ 1. The model is given the ``sandbox`` tool — a Python environment with

+ ``urllib``/``pandas``/``matplotlib`` and a writable working directory.

+ 2. It fetches the ticker's daily closing prices from a **pinned** data source

+ (Yahoo Finance's v8 chart JSON endpoint), writes them to ``prices.csv``,

+ and renders a line chart to ``chart.png``.

+ 3. Both files are saved to the sandbox workspace, which the Agent API exposes

+ as downloadable **artifacts** (``share_file`` output items).

-We poll the request until it completes, pull the CSV out of the sandbox's

-stdout (``sandbox_results.results[].stdout``), save it, and render the line

-chart locally with matplotlib.

+We poll the request to completion, read the shared files off the response, and

+download the CSV and PNG. This script has **no third-party dependencies** — it

+only speaks raw HTTP.

Why this shape?

- The ``sandbox`` tool is rejected on the synchronous/streaming path

("streaming failed: ... unknown tool"); it must run with ``background: true``

and be polled by id. This script always does that.

-- ``sandbox_results`` carries only text (code/stdout/stderr) — there is no

- binary artifact channel — so the chart is rendered on this side, and you

- also keep a reusable ``.csv``.

-- Top-level ``finance_search`` returns only the latest quote (no history) on

- the current deployment, so the price *series* is gathered from inside the

- sandbox. Because that relies on third-party web data, it is best-effort:

- the script retries the whole call a few times until it gets a usable CSV.

+- The sandbox now creates files. Anything written to the workspace comes back

+ as a ``share_file`` output item (``file_id`` + a ``/v1/responses/{id}/files/

+ {file_id}/content`` url); you can also list them via

+ ``GET /v1/responses/{id}/files``. So both the CSV and the chart PNG are

+ downloaded directly.

+- **Latency: pin the data source.** The slow part of an unconstrained sandbox

+ run is the model *discovering* a working price source (public pages 429 or

+ gate behind captchas). Telling it to hit Yahoo's v8 chart JSON endpoint

+ directly turns a multi-call hunt into a single fetch, which also leaves token

+ budget for rendering the chart in the same session.

+- **``finance_search`` has no history.** The top-level ``finance_search`` tool

+ returns only the *latest quote* (a single row) on the current deployment — it

+ cannot produce a price *series* — so the history is fetched in the sandbox.

The Agent API is called over **raw HTTP** (no SDK) so the request body — and

the sandbox tool in it — is fully visible, and the endpoint is configurable

@@ -41,12 +50,11 @@

import csv

import json

import os

-import re

import sys

import time

import urllib.error

import urllib.request

-from datetime import datetime

+from datetime import datetime, timezone

from pathlib import Path

from typing import Dict, List, Optional, Tuple

@@ -54,12 +62,17 @@

DEFAULT_BASE_URL = "https://api.perplexity.ai"

RESPONSES_PATH = "/v1/responses"

-CSV_START = "===CSV_START==="

-CSV_END = "===CSV_END==="

+# Filenames the sandbox is told to produce, matched on the way back by suffix.

+CSV_NAME = "prices.csv"

+PNG_NAME = "chart.png"

+# Yahoo's v8 chart JSON understands these range tokens directly; anything else

+# is expressed as an explicit period1/period2 window instead.

+YAHOO_RANGES = {"1d", "5d", "1mo", "3mo", "6mo", "1y", "2y", "5y", "10y", "ytd", "max"}

-# Friendly --period values mapped to a natural-language phrase the model can

-# act on. Anything not in this map is passed through verbatim.

+

+# Friendly --period values mapped to a natural-language phrase (used in logs /

+# the chart title). Anything not in this map is passed through verbatim.

PERIOD_PHRASES: Dict[str, str] = {

"1mo": "the past 1 month",

"3mo": "the past 3 months",

@@ -70,30 +83,40 @@

}

-SYSTEM_PROMPT = f"""You run inside a Python sandbox that includes the

-`perplexity` SDK (web search and URL fetch) plus pandas and the standard

-library. Your job is to produce a CSV of a stock's daily closing prices.

-

-Approach:

-- Use the perplexity SDK to obtain the daily closing prices: search the web

- and/or fetch a historical-price page that exposes a clean date/close table.

-- If a source fails or is rate-limited, try a different one. Do not give up

- after a single failure.

-- Print ONLY the final CSV to stdout, wrapped exactly between these fences:

- {CSV_START}

-

- {CSV_END}

- Header must be `date,close`; one row per trading day; sorted ascending by

- date; dates as YYYY-MM-DD; close as a plain number. Put no logs, debug

- output, or commentary inside the fences.

-

-Never fabricate or interpolate prices — use only values you actually

-retrieved."""

+SYSTEM_PROMPT = f"""You run inside a Python sandbox with a writable working

+directory that includes `urllib`/`requests`, `pandas`, `matplotlib`, and the

+standard library. Your job is to produce two files: a CSV of a stock's daily

+closing prices and a line chart of them.

+

+The two files ARE the deliverable. The task is complete only once `{CSV_NAME}`

+and `{PNG_NAME}` exist in the working directory — they are returned to the

+caller as downloadable artifacts. Do not end your turn with a text answer in

+place of the files.

+

+Steps:

+1. Fetch the daily closing prices from the EXACT URL you are given (Yahoo

+ Finance's v8 chart JSON), sending a browser `User-Agent` header such as

+ `Mozilla/5.0`. Parse `result.timestamp` (epoch seconds) together with

+ `result.indicators.quote[0].close`; drop any null closes. If that request

+ fails or is rate-limited, fall back to the Stooq daily CSV

+ (`https://stooq.com/q/d/l/?s=.us&i=d`) and filter to the window.

+ Never fabricate or interpolate prices.

+2. Write the data to `{CSV_NAME}`: header `date,close`; one row per trading

+ day; sorted ascending by date; dates YYYY-MM-DD; close as a plain number.

+3. Render a closing-price line chart with matplotlib (headless `Agg` backend)

+ and save it to `{PNG_NAME}`:

+ - figure ~10x5 inches at 150 dpi

+ - a single line in color #1f77b4, ~1.6pt wide, with a light fill below it

+ - dashed gridlines, x-axis label "Date", y-axis label "Close (USD)"

+ - the exact title you are given

+ - concise, auto-spaced date ticks on the x-axis

+4. Verify both files exist, then print only a one-line confirmation."""

PROMPT_TEMPLATE = (

- "Produce the daily closing-price CSV for {ticker} over {period_phrase}. "

- "Print it to stdout between the {start} / {end} fences."

+ "Fetch this exact URL for the daily closing prices: {url}\n"

+ "Write {csv} and render {png} for {ticker} over {period_phrase}. "

+ 'Title the chart exactly "{ticker} closing price — {period_label}".'

)

@@ -141,7 +164,7 @@ def _request(

headers={

"Authorization": f"Bearer {key}",

"Content-Type": "application/json",

- "User-Agent": "api-cookbook-finance-chart-sandbox/1.0",

+ "User-Agent": "api-cookbook-finance-chart-sandbox/3.0",

},

method=method,

)

@@ -155,6 +178,21 @@ def _request(

return err.code, {"error": {"message": err.reason}}

+def _download(base_url: str, key: str, url_or_path: str, timeout: int = 120) -> bytes:

+ """GET a file's raw bytes from an absolute URL or a base-relative path."""

+ url = url_or_path if url_or_path.startswith("http") else base_url + url_or_path

+ req = urllib.request.Request(

+ url,

+ headers={

+ "Authorization": f"Bearer {key}",

+ "User-Agent": "api-cookbook-finance-chart-sandbox/3.0",

+ },

+ method="GET",

+ )

+ with urllib.request.urlopen(req, timeout=timeout) as resp:

+ return resp.read()

+

+

def _poll(base_url: str, key: str, response_id: str, deadline: float) -> dict:

"""Poll a background response until terminal status (resilient to 5xx)."""

url = f"{base_url}{RESPONSES_PATH}/{response_id}"

@@ -170,11 +208,41 @@ def _poll(base_url: str, key: str, response_id: str, deadline: float) -> dict:

return body

+def yahoo_chart_url(

+ ticker: str, period: str, start: Optional[str], end: Optional[str]

+) -> str:

+ """Build the Yahoo v8 chart JSON URL for the ticker over the window.

+

+ Uses a ``range`` token for the standard lookback periods; an explicit

+ ``period1``/``period2`` epoch window for date ranges or non-standard

+ periods.

+ """

+ base = f"https://query1.finance.yahoo.com/v8/finance/chart/{ticker.upper()}"

+ if not start and not end and period in YAHOO_RANGES:

+ return f"{base}?range={period}&interval=1d"

+

+ def _epoch(date_str: str) -> int:

+ return int(

+ datetime.strptime(date_str, "%Y-%m-%d")

+ .replace(tzinfo=timezone.utc)

+ .timestamp()

+ )

+

+ p1 = _epoch(start) if start else 0

+ # +1 day so the end date itself is included.

+ p2 = _epoch(end) + 86400 if end else int(time.time())

+ return f"{base}?period1={p1}&period2={p2}&interval=1d"

+

+

def run_sandbox_request(

base_url: str,

key: str,

ticker: str,

+ period: str,

+ period_label: str,

period_phrase: str,

+ start: Optional[str],

+ end: Optional[str],

model: str,

max_steps: int,

poll_timeout: int,

@@ -184,14 +252,19 @@ def run_sandbox_request(

"model": model,

"instructions": SYSTEM_PROMPT,

"input": PROMPT_TEMPLATE.format(

+ url=yahoo_chart_url(ticker, period, start, end),

ticker=ticker.upper(),

+ period_label=period_label,

period_phrase=period_phrase,

- start=CSV_START,

- end=CSV_END,

+ csv=CSV_NAME,

+ png=PNG_NAME,

),

"tools": [{"type": "sandbox"}],

"background": True,

- "max_output_tokens": 4096,

+ # Headroom: the sandbox spends output tokens writing the code that

+ # fetches the data and renders the chart; a tight cap can starve the

+ # file-writing step.

+ "max_output_tokens": 8192,

"max_steps": max_steps,

}

status, body = _request(

@@ -205,60 +278,53 @@ def run_sandbox_request(

# ---------------------------------------------------------------------------

-# Response parsing

+# Files the sandbox produced

# ---------------------------------------------------------------------------

-def _sandbox_stdout(response: dict) -> str:

- """Concatenate stdout from every sandbox execution result."""

- chunks: List[str] = []

- for item in response.get("output", []) or []:

- if item.get("type") != "sandbox_results":

- continue

- # Real shape nests executions under `results`; tolerate a flat shape.

- results = item.get("results")

- if results:

- for res in results:

- if res.get("stdout"):

- chunks.append(res["stdout"])

- elif item.get("stdout"):

- chunks.append(item["stdout"])

- return "\n".join(chunks)

-

-

-def _message_text(response: dict) -> str:

- """Concatenate assistant ``output_text`` blocks."""

- chunks: List[str] = []

- for item in response.get("output", []) or []:

- if item.get("type") != "message":

- continue

- for block in item.get("content", []) or []:

- if block.get("type") == "output_text" and block.get("text"):

- chunks.append(block["text"])

- return "\n".join(chunks)

+def shared_files(response: dict, base_url: str, key: str) -> List[Dict[str, str]]:

+ """List files the sandbox shared, as ``[{filename, url}]``.

-

-def extract_csv(response: dict) -> Optional[str]:

- """Find the fenced CSV in the sandbox stdout, then the message text.

-

- Returns the CSV body (without fences), or None if nothing usable is found.

+ Prefers the ``share_file`` items embedded in the response ``output`` (they

+ carry a ready download ``url``); falls back to ``GET /v1/responses/{id}/

+ files`` and constructs the content path.

"""

- fence = re.compile(

- re.escape(CSV_START) + r"\s*(.*?)\s*" + re.escape(CSV_END), re.S

+ files: List[Dict[str, str]] = []

+ for item in response.get("output", []) or []:

+ if item.get("type") == "share_file" and item.get("url"):

+ files.append({"filename": item.get("filename", ""), "url": item["url"]})

+ if files:

+ return files

+

+ response_id = response.get("id")

+ if not response_id:

+ return files

+ status, body = _request(

+ "GET", f"{base_url}{RESPONSES_PATH}/{response_id}/files", key, None, timeout=60

)

- for haystack in (_sandbox_stdout(response), _message_text(response)):

- match = fence.search(haystack)

- if match and match.group(1).strip():

- return match.group(1).strip()

- # Fallback: a fenced ```csv block in the message.

- block = re.search(r"```csv\s*(.*?)```", _message_text(response), re.S)

- if block:

- lines = block.group(1).strip().splitlines()

- if lines and "date" in lines[0].lower():

- return block.group(1).strip()

+ if status >= 400:

+ return files

+ for item in body.get("data", []) or []:

+ if item.get("id"):

+ files.append({

+ "filename": item.get("filename", ""),

+ "url": f"{RESPONSES_PATH}/{response_id}/files/{item['id']}/content",

+ })

+ return files

+

+

+def pick_file(files: List[Dict[str, str]], suffix: str) -> Optional[Dict[str, str]]:

+ """Return the first shared file whose name ends with ``suffix``."""

+ for f in files:

+ if f.get("filename", "").lower().endswith(suffix):

+ return f

return None

def parse_csv(csv_text: str) -> Tuple[List[datetime], List[float]]:

- """Parse `date,close` CSV text into parallel lists, sorted by date."""

+ """Parse `date,close` CSV text into parallel lists, sorted by date.

+

+ Used to validate the downloaded CSV and report the series length — the

+ chart itself is rendered inside the sandbox.

+ """

reader = csv.DictReader(csv_text.splitlines())

if not reader.fieldnames:

raise RuntimeError("Empty CSV.")

@@ -287,37 +353,6 @@ def parse_csv(csv_text: str) -> Tuple[List[datetime], List[float]]:

return [r[0] for r in rows], [r[1] for r in rows]

-def render_chart(

- dates: List[datetime],

- closes: List[float],

- ticker: str,

- period_label: str,

- png_path: Path,

-) -> None:

- """Render a closing-price line chart to ``png_path``."""

- import matplotlib

-

- matplotlib.use("Agg") # headless: no display needed

- import matplotlib.pyplot as plt

- from matplotlib.dates import AutoDateLocator, ConciseDateFormatter

-

- fig, ax = plt.subplots(figsize=(10, 5))

- ax.plot(dates, closes, color="#1f77b4", linewidth=1.6)

- ax.fill_between(dates, closes, min(closes), color="#1f77b4", alpha=0.08)

- ax.set_title(f"{ticker.upper()} closing price — {period_label}")

- ax.set_xlabel("Date")

- ax.set_ylabel("Close (USD)")

- ax.grid(True, linestyle="--", alpha=0.4)

-

- locator = AutoDateLocator()

- ax.xaxis.set_major_locator(locator)

- ax.xaxis.set_major_formatter(ConciseDateFormatter(locator))

-

- fig.tight_layout()

- fig.savefig(png_path, dpi=150)

- plt.close(fig)

-

-

def sandbox_invocations(response: dict) -> int:

details = (response.get("usage") or {}).get("tool_calls_details") or {}

return (details.get("sandbox") or {}).get("invocation", 0) or 0

@@ -347,23 +382,27 @@ def build_period_phrase(

return period, PERIOD_PHRASES.get(period, f"the past {period}")

-def fetch_price_series(

+def fetch_chart(

base_url: str,

key: str,

ticker: str,

+ period: str,

+ period_label: str,

period_phrase: str,

+ start: Optional[str],

+ end: Optional[str],

model: str,

attempts: int,

max_steps: int,

poll_timeout: int,

on_attempt=None,

-) -> Tuple[List[datetime], List[float], str, dict]:

- """Run up to ``attempts`` background sandbox calls until a usable CSV parses.

+) -> Tuple[bytes, bytes, List[datetime], dict]:

+ """Run up to ``attempts`` background sandbox calls until both files come back.

- Returns ``(dates, closes, csv_text, response)``. Raises ``RuntimeError`` if

- no attempt yields a parseable ``date,close`` CSV. ``on_attempt(n, total,

- note)`` is an optional progress callback (``note`` is None at the start of

- an attempt, or a short failure reason).

+ Returns ``(csv_bytes, png_bytes, dates, response)``. Raises ``RuntimeError``

+ if no attempt yields a downloadable CSV+PNG pair with a usable series.

+ ``on_attempt(n, total, note)`` is an optional progress callback (``note`` is

+ None at the start of an attempt, or a short failure reason).

"""

response: dict = {}

for attempt in range(1, attempts + 1):

@@ -371,7 +410,8 @@ def fetch_price_series(

on_attempt(attempt, attempts, None)

try:

response = run_sandbox_request(

- base_url, key, ticker, period_phrase, model, max_steps, poll_timeout

+ base_url, key, ticker, period, period_label, period_phrase,

+ start, end, model, max_steps, poll_timeout,

)

except (RuntimeError, TimeoutError) as err:

if on_attempt:

@@ -383,21 +423,33 @@ def fetch_price_series(

on_attempt(attempt, attempts, f"request failed: {response.get('error')}")

continue

- candidate = extract_csv(response)

- if not candidate:

+ files = shared_files(response, base_url, key)

+ csv_file = pick_file(files, ".csv")

+ png_file = pick_file(files, ".png")

+ if not csv_file or not png_file:

+ have = ", ".join(f.get("filename", "?") for f in files) or "none"

if on_attempt:

- on_attempt(attempt, attempts, "no fenced CSV in output")

+ on_attempt(attempt, attempts, f"missing CSV/PNG (got: {have})")

continue

+

+ try:

+ csv_bytes = _download(base_url, key, csv_file["url"])

+ png_bytes = _download(base_url, key, png_file["url"])

+ except (urllib.error.URLError, TimeoutError) as err:

+ if on_attempt:

+ on_attempt(attempt, attempts, f"download failed: {err}")

+ continue

+

try:

- dates, closes = parse_csv(candidate)

+ dates, _ = parse_csv(csv_bytes.decode("utf-8", "replace"))

except RuntimeError as err:

if on_attempt:

on_attempt(attempt, attempts, f"unusable CSV: {err}")

continue

- return dates, closes, candidate, response

+ return csv_bytes, png_bytes, dates, response

raise RuntimeError(

- f"Could not obtain a usable price CSV from the sandbox after "

+ f"Could not obtain a usable chart from the sandbox after "

f"{attempts} attempt(s). Sandbox data fetching is best-effort "

"(third-party sources rate-limit); try more attempts or rerun."

)

@@ -407,7 +459,8 @@ def main() -> int:

parser = argparse.ArgumentParser(

description=(

"Plot a stock's closing-price history using the Perplexity Agent "

- "API sandbox tool (background task), rendered locally."

+ "API sandbox tool (background task). The sandbox fetches the prices "

+ "and renders the chart; both come back as downloadable files."

)

)

parser.add_argument("ticker", help="Ticker symbol, e.g. AAPL, MSFT, NVDA.")

@@ -424,11 +477,11 @@ def main() -> int:

"--attempts",

type=int,

default=3,

- help="Max background calls to try until a usable CSV comes back "

+ help="Max background calls to try until the chart comes back "

"(each is a separate sandbox session). Default 3.",

)

parser.add_argument(

- "--max-steps", type=int, default=25, help="Agent max_steps per attempt."

+ "--max-steps", type=int, default=15, help="Agent max_steps per attempt."

)

parser.add_argument(

"--poll-timeout",

@@ -468,16 +521,17 @@ def _log(attempt: int, total: int, note: Optional[str]) -> None:

if note is None:

print(

f"[attempt {attempt}/{total}] Asking the sandbox to fetch "

- f"{ticker} closing prices over {period_phrase}...",

+ f"{ticker} closing prices over {period_phrase} and plot them...",

file=sys.stderr,

)

else:

print(f" {note}", file=sys.stderr)

try:

- dates, closes, csv_text, response = fetch_price_series(

- args.base_url, key, ticker, period_phrase, args.model,

- args.attempts, args.max_steps, args.poll_timeout, on_attempt=_log,

+ csv_bytes, png_bytes, dates, response = fetch_chart(

+ args.base_url, key, ticker, args.period, period_label, period_phrase,

+ args.start, args.end, args.model, args.attempts, args.max_steps,

+ args.poll_timeout, on_attempt=_log,

)

except RuntimeError as err:

print(f"Error: {err}", file=sys.stderr)

@@ -486,13 +540,13 @@ def _log(attempt: int, total: int, note: Optional[str]) -> None:

if args.keep_json and response:

(out_dir / f"{slug}.json").write_text(json.dumps(response, indent=2))

- csv_path.write_text(csv_text + "\n")

- render_chart(dates, closes, ticker, period_label, png_path)

+ csv_path.write_bytes(csv_bytes)

+ png_path.write_bytes(png_bytes)

print(f"\nData points: {len(dates)} "

f"({dates[0]:%Y-%m-%d} → {dates[-1]:%Y-%m-%d})")

print(f"CSV: {csv_path}")

- print(f"Chart: {png_path}")

+ print(f"Chart: {png_path} (fetched and rendered in the sandbox)")

print(f"Sandbox invocations: {sandbox_invocations(response)}")

cost = total_cost(response)

if cost is not None:

diff --git a/docs/examples/finance-chart-sandbox/requirements.txt b/docs/examples/finance-chart-sandbox/requirements.txt

index 632e087..d1d59d8 100644

--- a/docs/examples/finance-chart-sandbox/requirements.txt

+++ b/docs/examples/finance-chart-sandbox/requirements.txt

@@ -1,2 +1,5 @@

-# The Agent API is called over raw HTTP (stdlib urllib) — no SDK needed.

-matplotlib>=3.7

+# No third-party dependencies.

+#

+# The Agent API is called over raw HTTP (stdlib urllib). The sandbox both

+# fetches the prices and renders the chart, so the CSV and PNG are downloaded

+# as files — this CLI needs nothing beyond the Python standard library (3.9+).

diff --git a/docs/examples/finance-chart-sandbox/webapp/app.py b/docs/examples/finance-chart-sandbox/webapp/app.py

index 0f3fd53..427b821 100644

--- a/docs/examples/finance-chart-sandbox/webapp/app.py

+++ b/docs/examples/finance-chart-sandbox/webapp/app.py

@@ -8,7 +8,8 @@

Phase 1 (data) A *background* Agent API request gives the model the

``sandbox`` tool, which resolves the ticker + period from

the question, fetches the daily closing prices inside an

- isolated container, and prints a META + ``date,close`` CSV.

+ isolated container, and **writes them to a CSV file**

+ (downloaded here) plus a tiny META block on stdout.

Phase 2 (answer) A *streaming* request (no sandbox) writes a short

natural-language analysis of that series, token by token.

@@ -26,7 +27,7 @@

Execution runs in a worker thread and writes incremental state onto the job, so

the SSE stream merely *tails* that state — reconnects never re-run the work.

-CSV-extraction/parsing helpers are reused from the CLI module

+CSV parsing and shared-file helpers are reused from the CLI module

(``finance_chart_sandbox``); only the API call differs (SDK here, raw HTTP there).

"""

@@ -59,34 +60,40 @@

_LOCK = threading.Lock()

DEFAULT_MODEL = "openai/gpt-5.5"

+POLL_TIMEOUT = 300

META_START = "===META_START==="

META_END = "===META_END==="

-# Phase 1: data-gathering inside the sandbox.

+# Phase 1: data-gathering AND charting inside the sandbox.

DATA_PROMPT = f"""You answer natural-language questions about a stock's recent

-price history by producing a chart-ready CSV.

-

-You have the `sandbox` tool — an isolated Python environment that includes the

-`perplexity` SDK (web search and URL fetch) plus pandas and the standard

-library.

-

-Do this:

-1. Read the user's question and determine the stock TICKER (resolve a company

- name to its symbol, e.g. "apple" -> AAPL) and the time PERIOD they asked

- about (default to the last 6 months if none is given).

-2. Use the sandbox to obtain the DAILY closing prices for that ticker over that

- period: search the web and/or fetch a historical-price page with a clean

- date/close table. If a source fails or is rate-limited, try another. Never

- fabricate or interpolate prices — use only values you actually retrieved.

-3. Print to stdout, in exactly this order and nothing else:

+price history by producing a CSV file and a line-chart PNG.

+

+You have the `sandbox` tool — an isolated Python environment with

+`urllib`/`requests`, pandas, matplotlib, the standard library, and a writable

+working directory.

+

+The files `{fcs.CSV_NAME}` and `{fcs.PNG_NAME}` ARE the deliverable; they are

+returned to the caller as downloadable artifacts. The task is complete only

+once both exist. Do this:

+1. Read the question and determine the stock TICKER (resolve a company name to

+ its symbol, e.g. "apple" -> AAPL) and the PERIOD as a Yahoo range token

+ (1mo, 3mo, 6mo, 1y, 2y, 5y; default 6mo).

+2. Fetch the daily closing prices from Yahoo Finance's v8 chart JSON at exactly

+ `https://query1.finance.yahoo.com/v8/finance/chart/?range=&interval=1d`

+ with a browser `User-Agent` header (e.g. `Mozilla/5.0`). Parse

+ `result.timestamp` (epoch) with `result.indicators.quote[0].close`; drop

+ null closes. If it is rate-limited, fall back to the Stooq daily CSV

+ (`https://stooq.com/q/d/l/?s=.us&i=d`). Never fabricate prices.

+3. Write `{fcs.CSV_NAME}`: header `date,close`; ascending; dates YYYY-MM-DD;

+ close a plain number.

+4. Render a line chart and save `{fcs.PNG_NAME}` (~10x5in @150dpi; line #1f77b4

+ with a light fill; dashed grid; x-label "Date", y-label "Close (USD)";

+ title " closing price —